- Home

- Contact

- Listings

- Luxury

- Selling

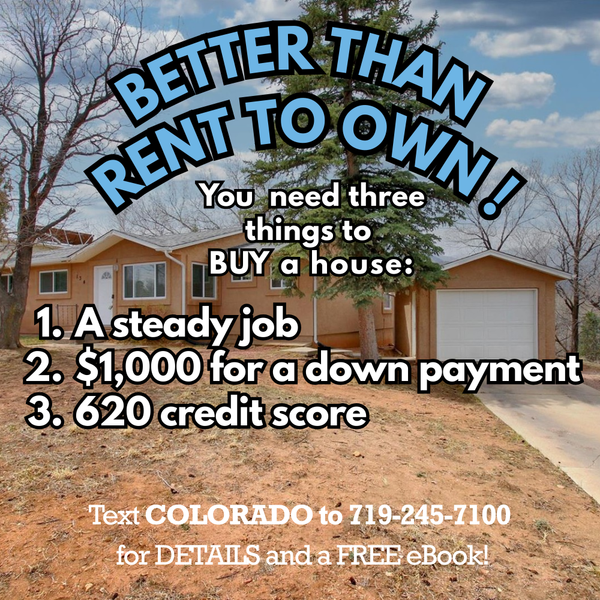

- Rent to Own

- Neighborhoods

- Briargate

- Flying Horse

- Cordera

- Cathedral Pines

- Broadmoor

- Kissing Camels

- Gleneagle

- East Colorado Springs

- Claremont Ranch

- Cimarron Hills

- Central Colorado Springs

- Black Forest

- Banning Lewis Ranch

- Old North End

- Old Farm / Antelope Meadows

- Old Colorado City

- Northgate

- Mountain Shadows

- Wolf Ranch

- Widefield

- West Colorado Springs

- Wagon Trails

- Southwest Colorado Springs

- Springs Ranch

- Stetson Hills

- Security

- Rockrimmon

- Powers

- Pleasant Valley

- Pine Creek

- Peregrine

- Patty Jewett

- Paint Brush Hills

- Jackson Creek

- Meridian Ranch

- Woodmen Hills

- Schools

- News!

-

- Register

- Sign In

GET MORE INFORMATION

Thanks! I'll get back to you shortly.